Originally published in Accounting Today.

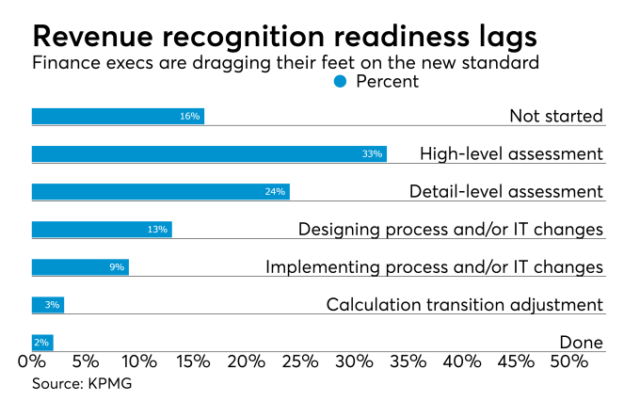

The rules governing revenue recognition for public and private companies worldwide are changing dramatically starting Jan. 1, 2018. And several recent surveys show that most companies are unprepared.

If you have not yet completed your implementation of the new revenue recognition standards — either ASC 606 or IFRS 15 — the following 10 lessons we have learned may help you get a jump start and utilize best practices that RGP, a finance and technology consultancy, and Zuora, which makes revenue recognition automation software, are seeing while helping companies transition to the new rules.

1. Just do it! Get started and keep up the momentum

Establish urgency now (since the new standard takes effect in less than a year for public companies, and a year later for non-public companies) and engage your stakeholders. Companies who are just starting will need full management support in order to meet the deadline. While 2018 seems sufficiently far away, it can easily take companies 15-18 months to transform their financial processes for the new rules. So it’s important to have a very detailed plan – including milestones and key dates – to manage the project and keep it on track. Some of the key decisions that need to be made early on can affect resources and requirements down the road. For example, deciding on the adoption date – and whether to offer a full retrospective presentation – can be challenging and will vary by priority for each stakeholder.

2. Get everyone in the same boat – engage cross-functional teams

Include top-level executive support to drive the project and ensure that people from the appropriate departments, which will ultimately include nearly all of them at some point, are involved at the right time in the project. Creating a steering committee is an important first step so that each organization can understand how the changes will affect their area and help guide the process. Their job will be to buy into scoping, and to make policy decisions that will impact the entire organization. Effective change management will help combat resistance from organizational politics related to budget and conflicting priorities across company departments.

3. Technology is key – select and implement a software solution

If necessary, use compliance with the new standard as an excuse to get the budget required for an automated revenue recognition solution such as Leeyo’s RevPro. Before selecting a system, define your business requirements carefully and be sure the vendor that you are choosing is ready for the standard with proven successful implementations. Be thoughtful about the number of use cases that are needed, and don’t forget about interdependencies with other systems such as ERPs, CRMs, and contract management, which could increase the complexity.

4. Technical accounting can be hard — interpret the guidance and make decisions

The new guidance is still being interpreted, particularly as it relates to commissions and contract modifications, and things like allocation of selling price. Moving to a principles-based standard adds significant judgment and estimates to the process. Despite your best intentions, your auditors, the SEC and the PCAOB may second guess your interpretation and judgment. In addition, while the FASB has said ASC 606 is not industry specific, the SEC has said that industries should implement the guidance in similar ways. Therefore, you need to keep current with what your peers are deciding. Along the way, you will want to monitor the activity of the FASB, including its transition resource group, as well as the AICPA, and discuss with your auditors, to ensure you stay on top of key developments. And finally, it’s more important than ever to document your policies and accounting positions in real-time.

5. It’s okay to be a control freak — implement processes and internal controls

Clearly with the new standard, your processes are going to have to change. Consider the completeness of your contracts. Do you have all material contracts and all the revisions? Also, who in the organization is applying judgment to estimates? Are they qualified? Under prior guidance, accountants could wait to report on things like variable compensation if they didn’t have a good estimate. Under the new standard, you need to report the estimates and then change them each period as they evolve. If not managed carefully, this could be perceived as earnings management or worse. To avoid issues, additional controls, such as review controls, may be necessary.

6. There’s a LOT of data — manage it

Eventually you are going to have to prove to your internal management and auditors that you have analyzed all the material revenue streams and contracts and come to the right conclusion. Therefore, best practice is to utilize relational database technology to link contracts with the analysis of the contract. Discuss documentation expectations with your auditors in advance. Some auditors even have templates they prefer to use for documentation. This can be a good starting point. Know what their expectations are for what the documentation should look like and timing for review.

7. Plan for disclosures early

Your level of disclosure is likely going to be a bit of a tug of war. On one hand, companies will try to limit information because it’s competitive and sensitive. On the other hand, more transparency is being demanded by the SEC, investors, and auditors. It will be a matter of pushing and pulling that will be resolved as time goes on. Work with your auditors and management to decide how much is enough, and what, if any, sensitive information should be included. Consider the disclosures required by the SEC for public companies (SAB 74) prior to adoption of a new standard as to when and how adoption will occur, along with information to allow investors to gauge the impact once effective.

8. Data gathering will take longer than you think

The process of gathering the right information can take significantly longer than expected. From scoping and selecting which contracts to review, to defining a process all the way through implementation, companies typically use either a top down or bottoms up approach, which defines the beginning level of detail. The difficulty in gathering data varies by company, but can be affected by the location and language of the contracts, whether they are oral or electronic, extent of additional contracts and modifications such as side agreements, and limitations on circulation due to confidentiality. Ensure time is built into your project plan for such setbacks.

9. Train and communicate on a need-to-know basis

Change management is an important aspect of a successful implementation. Decide which employees to train and when, across all levels and departments of your organization. Consider turnover, language and communication methods (particularly if you have a decentralized workforce) to ensure employees are being trained on the relevant aspects at the appropriate time. Be sure to include external stakeholders in your plan as well, since many will be interested in projected changes to revenue-driven metrics. Communication is critical for this kind of Finance transformation project that will touch so many areas of the organization.

10. Resources and talent may be scarce — plan for a sustainable future

These days, companies are being asked to do more with less, which has internal resources pretty busy. As the timeline shortens with the ever-approaching deadline, more resources will be necessary to meet the compliance date, and companies will find themselves competing for additional internal and external resources alike. Securing those resources as soon as possible is important. Begin with an evaluation of your internal team’s skills and availability, matching team members to identified workstreams. Then fill the gaps with new hires or external advisors. Likely, a mix of internal and external resources will be the most cost effective way to increase the skillset and hours required to ensure success of this one-time project.

Jagan Reddy is senior vice president of RevPro at Zuora.

Shauna Watson is head of RGP‘s global finance and accounting practice.